March 31, 2022

Stocks Dragged From The Boneyard

Market Recap & Boxscore

“Beware the Ides of March” was meant to warn Julius Caesar of his eventual assassination in Shakespeare’s play. However, it was an appropriate warning for short sellers this year. Following an initial 4.6% drawdown to start March, the 15th of the month marked the beginning of an 11-day, 11.3% recovery in the S&P 500 to finish the period up 5.6%. The TSX was positive 4.4%, while the MSCI World Index rose 4.9%.

In early March, the VIX Index, which measures the stock market’s expectation of volatility, reached levels not hit since October 2020. The short-term outlook was forbidding given the situation in Ukraine, the beginning of the Fed’s hiking cycle and a quarterly options expiry. But, the flashpoint for a rebound often occurs when doubt is deepest. As time passed without a downside surprise, hedges were forced to unwind and a reflexive upward thrust was released, the likes of which we have not seen since the COVID lows.

Commodities extended their march higher, with the Bloomberg Commodities Index rising 9.6%, and 30% year-to-date. The combination of oil’s weight in the index and its 13.3% rise in March helped propel the gauge, but agricultural and metals are significant contributors due to the supply chain disruptions caused by Russia’s assault on Ukraine. The Canadian dollar’s ascent was unbroken, gaining 2.2%. The loonie is restoring its petro-dollar label after being essentially static when oil prices rose from US$65 to over US$100.

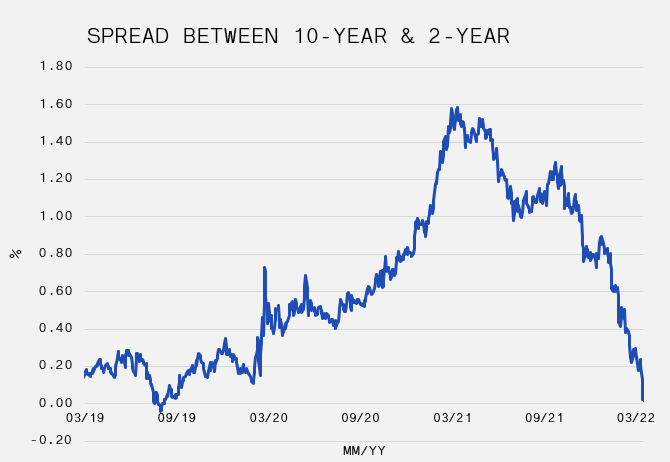

Outside of equities, action in the bond market remains volatile as the 10-year yield rose 53bps to 2.38%. The short end of the curve exhibited an even more dramatic move, with the 2-year rising 65bps to 2.35%, briefly flipping the difference between the 10-year and 2-year yield into negative territory. This negative yield curve is seen by many as a harbinger of recession due to its perfect track record since the 1980s, but as we’ve discussed numerous times the outlook was clear regardless of the inverted yield curve. With the nominal yield (2.38%) below the 10-year breakeven inflation (3%), the market was already pricing a growth slowdown over the next decade. With most of the action happening on the short-end, the market is declaring that an aggressive Fed will only accelerate the slowdown.

So, where does that leave us with the S&P 500 off 3.5% year-to-date? First, the bad news. Bonds are revealing that we’re likely to enter a recession in the next year. The Fed is intent on hiking into this downtrend, while commodities are gaining, employment is peaking, economic growth is cresting and the market is nearing all-time highs. However, the market doesn’t always reflect the economy, which was validated as recently as 2020. Opposing the bear view is the fact that economic growth and employment are strong, even if these are topping. Moreover, positioning among levered funds is now fairly tight after a deleveraging to start the year, real rates continue to be negative, indicating a loose environment, and most important, the recovery in risk assets despite a negative environment is indicative of a bull market. Finally, from a supply/demand picture, IPO supply is anticipated to be very low, while buybacks in the U.S. are currently approved at US$319 billion, compared to US$267 billion at the same point last year. Market pundits or news sources are too often pursued for forecasts and predictions, while the market’s ability to effectively price risk is regularly ignored. Currently, there is a wide range of uncertainty priced into the market. Accordingly, we respect the downside scenario, but also recognize that risk can be rewarded to the upside.