January 21, 2019

Staying The Course Proves Useful Early In New Year

Market Recap & Boxscore

So far in 2019, everyone, except the shorts, has made money. From global equity markets, to commodities, treasuries and gold, markets have started the year on a cautiously optimistic tone. Within equity markets, the TSX led the way up 8.5%, bolstered by a 17.5% appreciation in the price of oil. The S&P 500 followed suit, printing an 8.4% gain, while the MSCI World lagged with a still impressive 7.5% showing. Justification for the rebound include the easing of US-Chinese trade tensions, optimism that the US government shutdown is nearing an end and a possible slowdown in the Fed hiking cycle. However, we know full well that no single explanation can justify a rally, and the rationale for renewed optimism boils down to “the price is up.” While we do not rule out the re-testing of highs on the S&P 500, especially considering the unified level of pessimism built into market over the final quarter of 2018, we also cannot discount the importance the market has placed on commentary coming from an increasingly unpredictable Federal Reserve. Investors should tread carefully in 2019, but keep in mind that the past three months have highlighted that maintaining exposure to potential upside surprises is prudent, especially when the headlines suggest running for the exits.

Oil seemed to reach a near-term bottom when it briefly touched $42.50 in Dec-18. Since then, it rallied 26.8% in just under a month to $53.90 as of 21-Jan-19. While there has been commentary regarding OPEC’s planned supply cuts, the more important driver has been the continued rig count reduction in US Shale regions. On 18-Jan-19, Baker Hughes reported a 25-rig reduction in the US, representing a 2.4% decrease. However, the rig count is still up 14% year-over-year. Further, for the week ending 11-Jan-19, the EIA estimated US production to be a record 11.9 million barrels per day. Accordingly, we would not forecast an imminent rise to $100. Nevertheless, low oil prices and higher interest rates are two primary factors that will weaken the region. With the oil price now rising and rate increases taking a breather, the renewed optimism may have created an opportunity for profit-taking and right-sizing positions ahead of a more long-term trend.

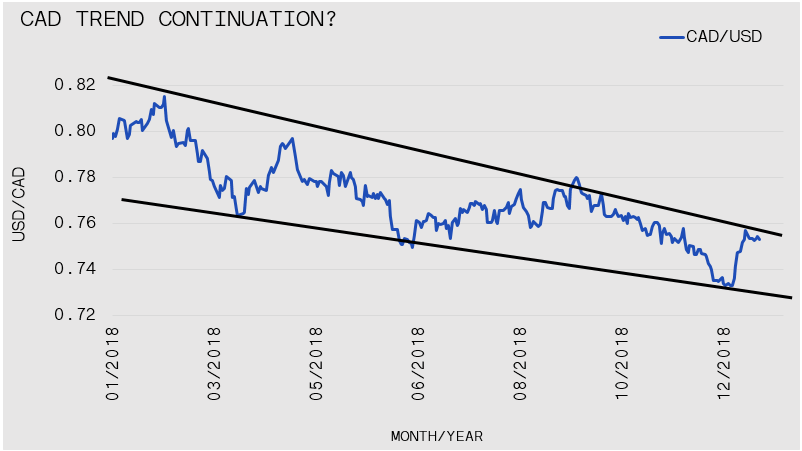

The Canadian dollar benefitted from the aforementioned commodity strength, climbing 1.7% over the past month and reversing a prolonged period of weakness since mid-2018. The sharp rebound has caused CAD to trade near the upper-end of its 2018 range; but it could be ripe for a pullback, especially considering recent fundamental news. The Financial Post reported that Canadians owe nearly $1.78 in debt for every $1 in disposable income. This regrettable situation is likely weighing on housing according to CREA, the average home price fell 4.9% in 2018. Also, in December, a US hedge fund, Crescat Capital, reported that over 80% of nonfinancial corporations in Canada reported negative free cash flow in the past twelve months. Looking forward, the prospects for a stronger loonie rest on continued vitality in oil prices or a reversal in the US Federal Reserve’s interest rate course. Otherwise, the overextended consumer, struggling corporations and a dovish Bank of Canada suggests that the movement will be to the downside.

Elsewhere in commodities, gold continued its upswing, bumping-up 1.6% to $1,280 and marking five consecutive months without a monthly drop, corresponding to a cumulative 10% surge since its July 2018 low. There are many factors converging in gold’s favour, namely the perceived Fed reversal (or at least a pivot to dovish policy), tepid inflation and a general rise in political risks and market volatility. However, gold’s breakout has been less tied to 10-year Treasury yields and the price of copper. Copper’s many industrial capacities link it to economic activity. Accordingly, copper prices often signal opposite trends for gold. Similarly, Treasury yields will fall along with copper prices when a downtrend is anticipated. This phenomenon has been on display since Sep-18, as the US 10-year yields fell from 3.23% to 2.68% as of Dec-18. However, since the calendar turned, copper has rallied 5.9% while gold seems to be flattening and longer-term bond prices have fallen. Meanwhile, equity markets have rebounded from a hellish December. Correlations and causations may be murky, but this turn of events highlights the risks of committing to an exclusively bearish strategy – sometimes the road not taken is the better choice.