October 29, 2018

October Slump Flattens Market for the Year

Market Recap & Boxscore

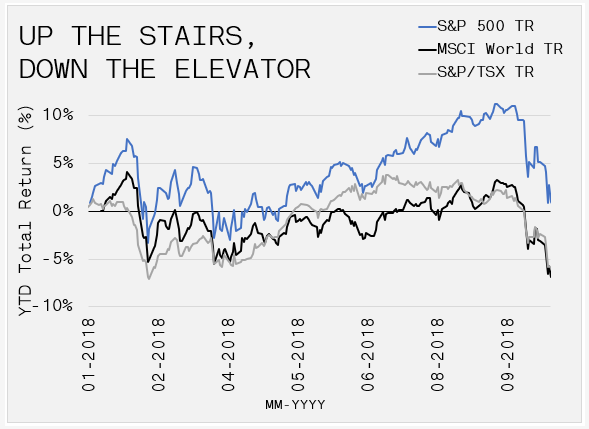

“Markets take the stairs up and the elevator down.” While many were starting to believe that the upward sloping stairs may last forever, October brought a harsh reality to market participants, with the S&P 500, MSCI World, and TSX down 9.6%, 9.6% and 8.2%, respectively. Rising rates, trade wars, and emerging market narratives contributed to the downside momentum. But the concerns expressed by management teams in third quarter earnings calls accelerated the slide. A constant drumbeat of increased cost pressure has tempered expectations for earnings growth, despite approximately 77% of companies beating expectations thus far. Earnings have been lifted by tax cuts and cost cutting – many firms have reduced expenses to year 2008-levels. As a result, options for earnings growth come down to good, old-fashioned revenue growth. Consequently, the true strength of the economy will have to come to the forefront.

Offsetting equity weakness, traditional protection mechanisms acted as-expected during the month, as the US 10-year bonds strengthened, and gold finally caught a bid. Gold was up 3.4% during the month, while the US 10-year yield has come back from 3.25% to 3.08%. Also pressuring longer-term yields was a weaker-than-expected US GDP print. It was revealed that government spending and inventory building was responsible for growth, rather than strong consumer demand.

Oil stumbled during the month, with WTI oil prices leaking by 11.5%. We commented previously on the incredible long bias in oil markets over the past few months. Though it is impossible to time when market positioning can reverse, the sensitivity to downside moves was witnessed in October. The backdrop for bullish sentiments was the combination of US sanctions on Iranian exports (effective 04-Nov-18) and persistent turmoil in Saudi Arabia. However, worries about slowing global GDP growth and Russian comments regarding maintaining production, were the catalysts for the recent selloff. Whether its oil or any other market, this month’s move shows that while timing a reversal is often futile, reducing exposure is ever-important when a good run becomes tired.

Beyond long-term rates, Central Bank maneuvers on both sides of the North American border had large implications on the short-end of the yield curve. Following the US Federal Reserve’s 25bp increase on 26-Sep-18, Canada followed-suit in October. Governor Poloz signaled confidence in the economy with a 25bp increase in the benchmark rate, which now rests at 1.75%. The removal of uncertainty around the revised trade agreement with the US and Mexico was also declared as a reason for rates to rise towards the stated neutral rate of 2.5% to 3.5%. Even though rates remain at historically low levels, the consumers’ capacity to withstand sequential rate increases is questionable due to household debt levels in Canada. A recent Bloomberg article cited that Canadian household credit growth was 3.6% in September year-over-year, the slowest since 1983 and below the 8.1% historical average. While the data is only representative of one month, it could indicate that Canadians are unable to add incremental leverage at higher interest rates. Now more than ever, credit growth acts as a primary indicator of GDP strength so it will be interesting to observe the data point’s impact on the Canadian economy and the prospects for further rate increases.

The Bank of Canada and its Governor, Stephen Poloz, carry out monetary policy by raising and lowering the target for the overnight rate. In the US, the Federal Open Market Committee has similar responsibility. However, there is a growing impasse between President Trump, Fed Members such as Neel Kashkari of Minneapolis and the Federal Reserve. Those who oppose the Federal Reserve are lobbying for a pause in rate hikes and less monetary tightening. Low borrowing costs are needed to help prolong the growth cycle, especially since the Trump administration has already used its primary bullets (tax cuts and relaxed regulations) in the middle of midterm elections. This internal conflict will be an extra source of volatility as the world economy plateaus.