October 01, 2020

Election Outlook Obscures The Prospects for 4Q20

Third Quarter 2020 Newsletter

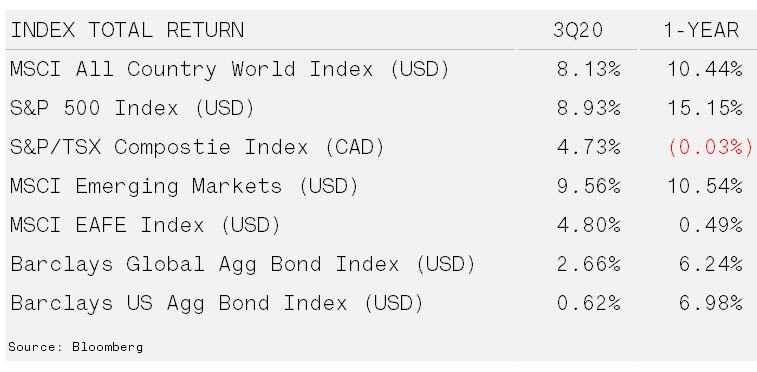

Bond Yields Firm As Domestic Equities Rally – Global equities gained in the third quarter but performance was uneven among geographic regions. Aggressive monetary and fiscal stimulus measures helped asset prices in the United States while lockdowns in Asia neutralized COVID-19 and fueled markets.

As fiscal stimulus measures ran their course and children returned to school in September risk appetites slipped. U.S. markets fell 4%-6% during the month but are equivalently within all-time highs. European equities were flat-to-down as exposure to underperforming financial and energy sectors prevented gains. Despite heavy weights to similar sectors, the Canadian S&P/TSX Composite advanced nearly 5% as metals, mining and other commodity related equities surged.

Most commodities received a bid as the U.S. dollar fell against major currencies (excluding the Yen). Lumber attracted most of the limelight as it broke through previous highs, topping out at $1,000 before finishing the quarter at $612, gaining 41%. Oil prices were the first commodity to falter, ending the quarter flat after peaking at the end of August.

Gold drifted higher but came under pressure as bond yields began to firm and the U.S. dollar found a temporary bottom. Higher bond yields without inflation will limit gold’s upside and likely upset equity valuations.

The Implications of Elections – Conventional wisdom says that uncertainty is bad for markets. Intuitively this makes sense since confidence in an outcome, or at the very least a stable outlook, should lead to more investment decisions today. With the U.S. election (03-Nov-20) just around the corner equity markets have started pricing in the risk of political instability. This is most evident in the VIX (Volatility) Index, which has anticipated a period of uncertainty in the fourth quarter since the market decline in March. This marked a turning point for expectations about the election’s outcome. President Trump could no longer use the stock market as the gauge for his success during the Coronavirus Crash.

Despite the stock market recovery, the mishandling of the outbreak has cast the Democrats into a healthy lead. Forecasts are now suggesting a Blue Wave will give Joe Biden the presidency and both houses of Congress to the Democrats. A “sweep” may unsettle the market because of the absence of the checks and balances that demand negotiation and compromise, which pulls either wing toward the centre. Instead swift, self-serving decisions may present themselves over important rulings such as the current anti-trust recommendations for big-technology firms. The Democratically controlled House of Representatives just released a massive overhaul that would have major consequences for the largest publicly traded companies, Amazon and Apple. This type of change could be a major catalyst that causes a change in market leaders as we highlighted in our October 2019 newsletter.

Nevertheless, declaring a loss for Trump and the Republicans is still premature. The possibility remains that the gap can be overcome, or it can be tightened enough to contest the election results. A contested election could arise from a simple delay in counting of mail-in ballots or a more serious scenario such as voter fraud. The U.S. presidential election in 2000 was contested when close results in Florida led to a vote recount by hand. The recount ended up in the 9-person Supreme Court. While a delay similar the Bush-Gore controversy may disrupt markets in the short-term, more worrying are the results of a recent Hofstra University survey. This survey showed a significant rise in the number of Americans, both Democrats and Republicans, who feel it is justified for their party to use violence to advance political goals.

While election outcomes and legislation can have adverse impacts on specific cohorts of markets, in general equity markets typically prosper regardless of the political party in office. Studying historical returns, if you exclude the most recent 16 years, the correlation between presidential party and stock market returns is non-existent. The Great Financial Crisis and subsequent rebound sway the results slightly in favour of the Democrats. However, most evident is that returns have more to do with the business cycle than presidents.

Our tactical decision-making process is more aligned with the business cycle than election outcomes. These maneuvers are smaller in nature to strategic allocation decisions, which align with client risk tolerances, but these are never single point decisions. Factors such as valuation, fundamentals and technical indicators are also incorporated into investment decisions. Take big-technology firms, we view the proposed anti-trust investigation combined with valuations as a major concern but are respecting the strong fundamentals and technical price charts.