Yes, the Dollar is Still King

Fed Sets Sight on Fighting “Transitory” Inflation – Markets followed up a brutal second quarter with more losses. The persistent inflationary forces discussed here, and once thought to be transitory, have put the U.S. Federal Reserve and other central banks in a box. While inflation has pulled back from 9.1% in June, a 40-year high, levels have remained elevated forcing the Federal Reserve to raise interest rates in 2022 faster than any other time in recent history.

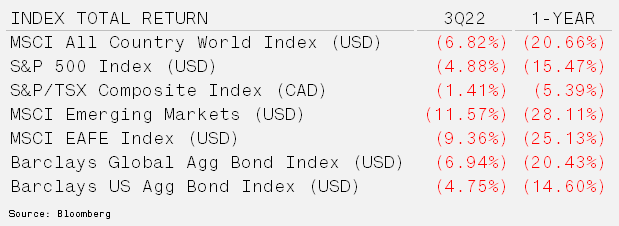

Traditional safe havens continue to be anything but. Gold fell 8.2% versus the U.S. dollar while long-term US Treasuries fell over 10% for the quarter. The U.S. dollar is a lone standout, gaining about 7% for the quarter as geopolitical and economic stability have taken a decisive turn toward vulnerability.

The Return of the Global Wrecking Ball – The U.S. dollar has risen to levels not experienced in over 20 years. The primary cause of the quick ascent by the world’s reserve currency has been the rapid increase in short-term interest rates. By increasing borrowing rates, the U.S. Federal Reserve is hoping that demand destruction will lead to lower inflation. But with 62% of the world’s currency reserves held in U.S. dollars, a soaring greenback impacts nearly every market.

The strength of the U.S. economy, with its stability and openness to trade and capital flows as well as the rule of law drove the dollar’s status as a global reserve currency. Post World War II, the Bretton Woods arrangement forced central banks abroad to accumulate reserve dollars which they could use to stabilize their currencies in the event of a crisis. While most fiat floats on global markets today, reserves are still used to aid in financial stability through foreign exchange markets as well as trade.

Over 85% of international transactions involve the U.S. dollar. The greenback is the predominant currency unit in which global commodity markets are quoted, traded and settled. When combined with the demand for global reserves, the path of least resistance for the world’s reserve currency is naturally higher. To offset this pressure, the foreign entities can reinvest their trade surpluses into dollar-denominated assets, like bonds valued in dollars and traded on U.S. markets. As a result, foreign investors now hold $28 trillion in dollar-denominated assets.

As the dollar increases in strength it has several knock-on effects that help to slow its advancement further. Commodities for example become more expensive to foreign countries if the U.S. dollar is increasing relative to their currency. This slows investments in raw materials and eventually roles into the manufacturing sector as not all price increases can be pushed through. The benefit for the U.S. is on the inflation side, as there is slowing commodity demand along with increasing purchasing power.

U.S. corporations are however negatively impacted by an increasing dollar. An estimation from Morgan Stanley shows that the profit margin of U.S. companies will fall 0.5% for every 1% increase in the dollar. This is because most corporations have overseas operations and when sales from those subsidiaries are transferred back for reporting purposes, they are worth less.

A third area that is negatively impacted by a rising U.S. dollar are global debt markets. Foreign currency debt, debt issued by firms in a currency other than that of their home country, is also dominated by the greenback. The U.S. dollar accounts for 60% of outstanding debt securities globally, well ahead of the euro, whose share is 23%. If debt is difficult to service, this can slow lending and the economy.

The U.S. dollar remains a dominant and relatively stable currency as it has leveraged its store of value function across global reserves, trade and debt markets. Meanwhile, the U.S. remains the deepest financial market in the world where rule of law exists. GAVIN will continue to have a meaningful allocation to the U.S. dollar. This occurs through publicly listed securities, real estate or private investments. Since the start of 2022, the dollar index has soared nearly 16%, the largest yearly percentage gains since at least 1972. Dollar demand remains strong and accelerates during a global economic slowdown.

Investment Management