Stocks Deny The Hardship In The Economy

We will describe the disorder of investing in 2020 before disclosing the market return data during the past month.

First, on 21-May-20, another 2.4 million US citizens filed for unemployment in the previous week, bringing the total to nearly 39 million. An additional 1.1 million Americans sought jobless claims under a new ‘temporary Pandemic Unemployment Assistance Program’ so headline numbers are in fact understated.

Next, tensions with China continue to mount. Evidently, this rivalry will become Trump’s primary focus ahead of November’s election. China’s handling of Covid-19 and the embattled trade deal are persistent aggravations for the enigmatic President. Additionally, China’s new national security bill that increases surveillance in Hong Kong has implications for the US. Hong Kong needs to retain enough autonomy to qualify for US tariff exemptions that are otherwise imposed on China. Also, in Asia, military skirmishes along the China-India border have been reported throughout May. Peace has largely existed between the two countries since their war in 1962. However, scuffles frequently erupt along the 3,488 km frontier that is generally disputed and indistinguishable.

How have these severe disturbances impacted equities? Well, a continuation of the rally, of course! Whether it is the US (+2.8%), Canada (+2.5%), or the MSCI Ex. US (+2.9%), global markets continue to grind higher and force bear after bear to hibernate. There are several reasons to justify a continuation of the bounce off the March low, including the cap-weighted nature of the S&P 500, whereby the largest constituents (ie. Microsoft, Apple, Amazon, Facebook) account for a disproportionate weight in the index’s price and underlying earnings. Tech, Healthcare, and Communications represent almost 50% of earnings for the index. These sectors are understandably less affected by the pandemic relative to the median US company. However, price action later in the month began to shift with sectors such as Financials, Industrials, Real Estate and Materials taking the lead while Tech and Healthcare lagged. Surely if the economy’s reopening is as smooth as the market’s rebound suggests, this trend will likely continue. Moreover, the potential for rapid and vibrant economic growth when the economy is fully reopened is conceivable given it is bolstered by trillions in Federal and monetary stimulus. Nevertheless, with so much economic uncertainty, the threat of a second wave of the virus and the S&P 500 hovering around key technical resistance points, we are focused on right-sizing exposures and ensuring adequate protection.

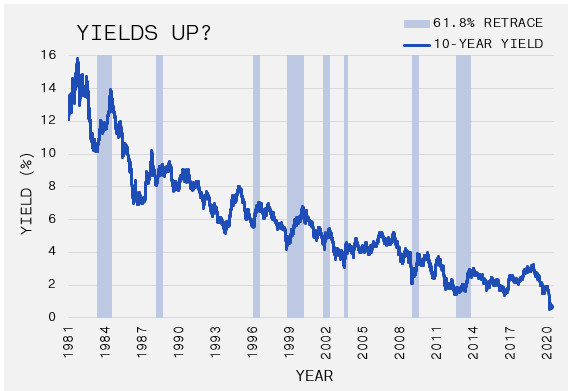

We regularly evaluate the bond market for insight on future cross asset movements. In May, longer-term US yields exhibited an upward trend. The corresponding chart (inspired by Jawad Mian of stray-reflections.com) maps the big decline in bond yields since the beginning of the secular downturn in rates from 1981. The shaded areas indicate each instance where the 10-year yield retraced 61.8% of its drop during the preceding 2 to 14-month period.

Today, the 10-year has fallen from a high of 3.2% to a low of 0.4% in March, which would pin a 61.8% retrace at 2.1%, with the midpoint date in 6-9 months.

If this forecast materializes as the model implies, whether it is prompted by real economic growth or a return of secular inflation, the knock-on effects may be considerable. It could reverse the duration trade that has supported equity markets throughout the bond yield’s historical descent; and, particularly, the fast growth-low profit stocks. Fears of higher rates would also impact the perceived credit quality of the US, whose debt position will swell due to the $4 trillion deficit in 2020. Rising rates will also affect the ability of corporations to service an unsustainable debt position, which has expanded by $834 billion through the end of April. Finally, percolating inflation may jolt commodity markets which have been fighting to get out of the dumpster for years.

This outcome is speculative at best, but the ingredients are certainly present for the scenario to play out. Further, the set-up is reinforced by massive monetary and fiscal stimulus, de-globalization, emerging cold war with China, onshoring of US jobs and the initiation of “just-in-case” inventory management. We will continue to be vigilant and active when evaluating the prospects for inflation (and deflation) to structure portfolios that protect and benefit in different environments.

Monthly Market Recaps