Solid US Stock Gains Among Rising US Bond Yields

The MSCI World and S&P 500 recorded solid gains in September, rising 0.8% and 0.6%, respectively, while the TSX lagged with a 0.7% drop for the month. Financials performed well in Canada following strong third quarter earnings, but weak gold (down 1.0%), NAFTA trade concerns and relative underperformance of Canadian Western Select Oil hurt the energy sector. Commodities in general were positive during the month as the Bloomberg Commodity Index rose 2.0%. Emerging Markets, reflected by iShares MSCI Emerging Markets Index (EEM) on the NYSE, caught a bid and stabilized after a 3.4% drop in August.

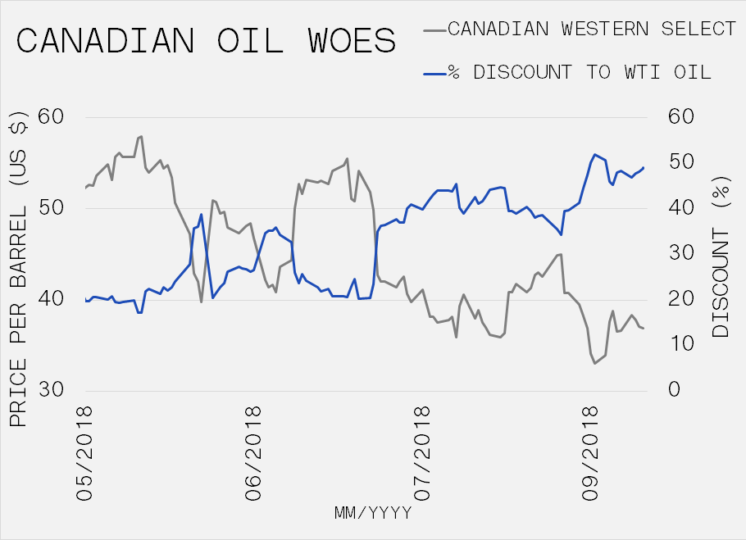

Oil continues to be a tale of two tapes – the main indices (Brent or WTI) versus Canadian Western Select. WTI and Brent were boosted during the month when OPEC commented that production would not increase to offset reductions from Iranian sanctions and Venezuelan turmoil. The decision came despite Trump’s Twitter plea for OPEC to expand supply. Given the military protection that the US provides to the Middle East, Trump declared that lower oil prices should be the implicit compensation. It is questionable whether civilians residing in Yemen, Iran, Iraq or Syria are enthusiastic about the US presence in their country. But politics aside, the US is expected to maintain hostile oil price rhetoric as the economic expansion enters the final innings. Western Select continues to lag as no progress is made on pipelines to move the product. Western Select registered a 14.1% drop in September as WTI prices were boosted by 3.8%. These movements brought the price differential between the two to $35.50, a 49% discount. Correspondingly, Canadian producers are being clobbered and a major factor in the TSX’s weakness during the month.

The 30-year US Treasury Bond yield matched the May 2018 highs and moved decisively above 3% to 3.25% in September. The US Federal reserve not only increased the discount rate at their scheduled meeting, but they ratcheted-up the target range of the Federal Funds Rate to 2-2.5%, signaled one more hike in December and three lifts in 2019. The 2 and 10-year yields also continue to rise, with the 2-year at 2.8% (up 89bps from Jan-19) and the 10-year at 3.1%. Yields ticked up into and on the news of the Federal Reserve decision but have since moderated. Beyond the news flow, it is interesting to monitor Treasury pricing in the context of the Federal Reserve’s initiative to shrink their balance sheet. The third quarter marked a planned increase in the amount of securities the Fed planned to roll off their balance sheet, up to $50 billion per month. The yield on the 30-year Treasury has risen considerably since this time, and a similar move can be observed in the 10-year. Uncertainty about the future is often an explanation for rising yields. The anticipation of large budget deficits, over supply of Treasuries, trade wars and tariffs promote uncertainty.

We will reference President Trump to summarize the current impasse in NAFTA negotiations. The President’s recent comments include the country’s displeasure with the Canadian negotiating style and a claim that he refused a one-on-one meeting with Prime Minister Trudeau. As negotiations are extended, concerns linger around issues such as trade dispute mechanisms and dairy, casting doubt on the Canadian dollar and certain sectors within the country, particularly auto parts manufacturers and lumber producers. Producers have repeatedly used the World Trade Organization trade dispute process to address anti-dumping complaints from the US and if the mechanism is altered, this could impact exports into the US, especially without a new Softwood Lumber Agreement in place.

Monthly Market Recaps