August 29, 2018

Repeating Themes Push Markets Higher in US and Canada

Market Recap & Box Score

Tariff talk once again helped boost the S&P 500’s relative performance versus global equity benchmarks. With a 3.1% gain in August, the S&P 500 outpaced both the MSCI World (1.0%) and TSX (0.8%). The MSCI World Index was affected by relative weakness in emerging markets and Europe; excluding the US, the index was down 1.1%. Softness in foreign markets was driven by US dollar (USD) strength to begin the month, as the DXY was up 2.2% and MSCI World down 3.7% through 15-Aug-18.

The USD has been buoyed by several factors; (1) rising interest rates in the US are diverging from the rest of the world, (2) tariff and protectionist policies, (3) shortage of USD overseas. The robust USD environment affects emerging market economies who have large US dollar debt service obligations and those that need to import USD-priced inputs and services. Europe also weakened due to Turkey’s political spat with the US that led to worries about sanctions and the impact on the country’s banking system. In addition, concerns in Italy continue to mount. Moody’s extended its review of the country’s bond rating and rumours suggested that Italy would seek additional ECB support to purchase its bonds. In Canada, a relatively benign commodity environment helped to suppress the TSX. Within commodities, oil registered positive results, rising 3.1% following a weak July, while gold and silver both were down. Gold’s woes have lingered for more than 6 months, dropping 11% from its high of $1,345 in February 2018. The US 10-year Treasury yield took a step back during the month, dropping 9bps to 2.87%, while the spread between it and the 2-year narrowed to 21bps.

NAFTA has been prominent in Canadian headlines. President Trump announced his intention to enter into a new bilateral US-Mexico trade agreement, which indirectly applies political pressure on Canada to succumb to US trade demands. Canada’s Minister of Foreign Affairs, Chrystia Freeland, has been in lengthy discussions with US representative, Robert Lighthizer, despite Trump’s posturing. Ms. Freeland’s history opposing Russian oligarchs helps provide some insight into her ability to withstand political pressure and bullying tactics.

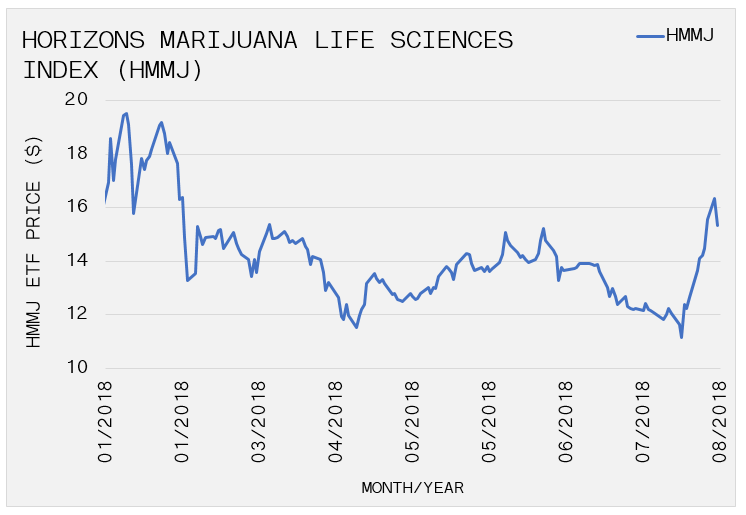

After a slow first half in 2018 and many cutting their losses in cannabis, a mid-August announcement from Constellation Brands suddenly sparked a rally that helped lift the sector 24% for the month. Constellation Brands (NYSE:STZ), sporting such brands as Corona and Modelo, followed an earlier $200 million investment in Canopy Growth Company (TSE: CGC) with a follow-on $3.8 billion investment. As part of the transaction, STZ will nominate four directors of the seven-member board, which allows the company control over CGC. Later, news broke that global spirit powerhouse Diageo (NYSE: DEO) was evaluating a potential investment in the space, helping to add fuel to the speculative fire. Many are now identifying names such as Pepsi, to Big Tobacco as potential acquirers in the future. The potential for M&A has, for the time being, caused prices and volumes to spike across the space and BNN Bloomberg to focus much of their attention on the topic. A constantly changing regulatory environment and greater disclosure on the medical benefit will inspire Big Pharma to enter the market. A joint research project between a Washington, DC based data analytics firm and London UK biotech firm reported that 7 of Canada’s top 10 cannabis patent holders are major multi-national pharmaceutical companies. With valuations in Canada already sky-high, either fundamental performance, or additional M&A will be needed to keep things moving.