May 29, 2018

Political Chaos in Italy

Market Recap & Box Score

Markets continued to grind higher in May, led by North America. The S&P 500 recorded a 1.5% gain, while the TSX advanced 2.2%, buoyed by continued strength in commodity companies despite relatively flat performance of their underlying commodities. The MSCI World Index lagged, albeit with a 0.3% gain. Political turmoil and the market’s next “Exit” story stole the headlines in Europe. Gold’s price movement was benign throughout the month, recording a 1% move on only one day, and ending the period down 0.5%.

Oil’s 0.3% price change concealed a volatile month, as the price plunged 7% over the final four trading days. Market participants who were long oil were spooked by Saudi Energy Minister Khalid Al-Falih’s speech in Russia, when he announced that supply caps could be scaled back and the possibility of supply increases. However, it will take a unilateral decision to enact any official supply increase out of OPEC and we anticipate continued volatility as news leaks. Markets will eagerly anticipate the results of the OPEC meeting on 22-Jun-18, while closely monitoring inventory numbers to determine whether the recent price above $60 has served to quell demand.

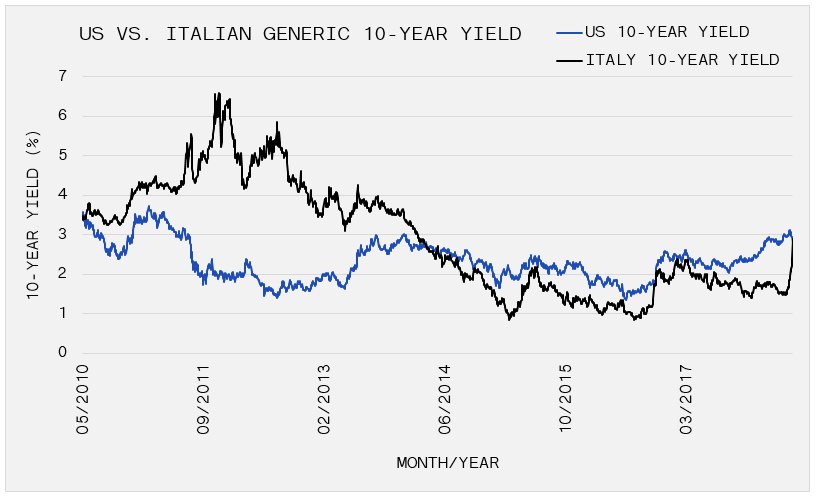

Volatility in equity and fixed income markets ramped up as political turmoil in Italy resurfaced another Euro-exit scenario. The Italian 10-year yield has been consistently below the US benchmark since crossing in early 2014. However, yields rose rapidly above 3% on 29-May-18 when populist Italian political parties failed to produce a new coalition government. At the same time, the US 10-year completed a 30bp retreat from its recent 3.1% high to 2.8%. While Italian credit is questionable at best, it is fairly easy to reconcile the yield differential given the European Central Bank (ECB) has purchased €341Bn of Italian bonds since 2012 and it continues to buy an additional €4Bn each month. One can also visualize the potential damage that an Italian exit could produce. We realize the risk is likely overblown, and there are constitutional hurdles present that make the result unlikely. However, we also understand the risk-reward tradeoff and continue to question whether the current 3% rate, or the 1.6% average rate since 2015 is anywhere close the reward required to compensate for the low likelihood event of potential default. With €2.3Tr of outstanding debt, a debt-to-GDP ratio of 132% and persistent political turmoil, investors are relying first on the ECB, and second on a political turnaround, to provide returns that still lag US government bonds.

Closer to home, the Liberal government’s decision to purchase Kinder Morgan Canada Ltd.’s Trans Mountain Pipeline expansion for $4.5Bn was a last-ditch effort to save the proposal. The pipeline will extend from the oil sands of Alberta to a port in British Columbia. It would allow Canadian crude to gain greater access to foreign markets and higher prices. The project adds a much-needed 590K barrels per day of capacity from the current 300K, which will ease some of the backlog in Canadian oil markets. Canada will retain key personnel from Kinder Morgan and begin the undertaking this summer, but will actively seek a buyer for the project.