November 29, 2019

Monitoring Spreads and Commodities for a Possible Reversal

Market Recap & Box Score

Coming into the seasonally strong end-of-year period, markets have so far toed the line. The S&P 500 (+3.5%), TSX (+4.2%) and MSCI (+3.0%) all posted strong gains in November. This marks a third consecutive month of strength for the S&P 500 and MSCI World Index as reduced impeachment risk and trade war optimism helped support the advances.

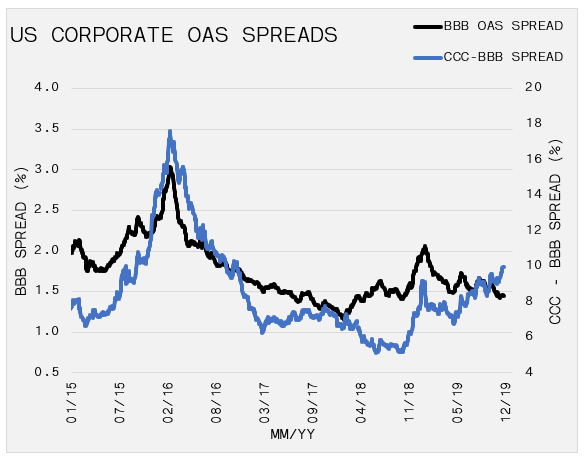

BNP Paribas recently reported that outflows from equity mutual funds and ETFs surpassed $150 billion during the past 6 months. Previous peaks in outflows occurred in 2016, 2011, 2008 and 2000 when markets were strikingly different than the all-time highs that are present today. As themarketear.com highlights, strong outperformance typically follows periods where outflows exceed $50 billion. Accordingly, the massive retail redemptions suggest that robust equity performance may persist. However, in this instance, negative fund flows could imply that markets are preparing to rollover. It is no secret that corporate buybacks have supported the upward momentum and that easy access to credit has funded the buybacks. At this point, the data does not indicate that the trend will reverse anytime soon. BBB and high yield issuers continue to have significant access to debt financing and spreads remain tight. Although, borrowers rated CCC and below have experienced widening spreads since Sep-18, but this portion of the market represents only 3% of US corporate debt outstanding. Comparatively, the BBB-B component of the market accounts for 66% of debt and most of the buyback flow. As a result, more attention is dedicated to the importance of the spread movements in those constituents.

The TSX index shrugged off a tough October to post a 4.2% gain for the current period, good enough to lead US and the MSCI Indexes. Energy rebounded slightly during the month as the sector increased 4.2%. However, the 9.4% improvement in the Tech sector paced the TSX. Constellation Software (TSE: CSU) jumped 9.8% for the month to all-time highs on strong earnings, while Shopify and CGI both registered convincing returns.

Thank you to Kevin Muir, the macrotourist, for drawing attention to Canada’s inverted yield curve. When the US yield curve first inverted in April, many declared that this signaled a looming recession. Since then, the US curve has steepened, helping to alleviate some worries. But, yields in Canada continue to be inverted which essentially demonstrates that short-term lending conditions are too tight in relation to expectations for slower long-term growth, or a future reduction. Nevertheless, Canadian economic numbers continue to surprise to the upside; as such, the yield curve remains uncharacteristic for bullish forecasts.

Commodities generally had a quiet month, as oil maintains the $50-60 range ahead of OPEC’s meeting in early December. Demand for oil has cooled in 2019 due to slowing global growth. Supply has been held in check by planned OPEC cuts which are set to expire in March 2020. There are many reasons to believe US oil production will taper at some point, but so far this has not been the case. Unless OPEC’s production cuts persist, oil prices will struggle in 2020. Nonetheless, on a rate of change basis, we note that late Dec-18 marked the low for oil at $46, a steep decline from $76 in Oct-18. So, while rangebound in 2019, on a year-over-year basis we are exiting a period of weakness into a period of strength, which could have implications on inflation expectations to begin 2020. Bond markets were beginning to sense this in October and November as the US 10-year yield rose 41bps to 1.94% on 11-Nov-19, but have since backed-up to 1.77%. Copper similarly fell in November after a strong month in October.

Copper and oil, along with the CRB US Spot Raw Industrials index, will be closely monitored for signs of inflation. Inflation is present and growing at the consumer level, but its impact has not yet obstructed corporate fundamentals (margins, input costs) or influenced Fed policy from a macro perspective. One underappreciated commodity that has “logged” impressive gains is lumber, soaring 27% from its May low. Falling mortgage rates in the US sparked the housing market and intensified demand for lumber.