April 28, 2022

Markets Bruised After Brutal April

Market Recap & Boxscore

Last month’s rally in equity markets quickly faded in April as aggressive and persistent selling led the S&P 500 and MSCI World indexes to declines of 7%. Even the TSX, which has defied gravity in 2022, fell 4.3%. Under the hood, the flight to safety accelerated with markets favouring staples, real estate and utilities, while selling discretionary, technology and financials. Unlike earlier in the year, downside participation by large cap Generals contributed to the weakness during the period. Index-dominating names like Google and Apple crumbled over 16% and 8%, respectively. We always keep a close eye on credit markets to confirm a move in equities. Yields across corporate bonds persistently marched higher, and spreads, as measured by the BofA US High Yield Index OAS, rose 51bps to 3.89%. The trend in credit spreads is notable, but we are not yet at levels of excess stress.

Commodities did not cooperate with the decisive downward moves in equities and bonds. The results were mixed across the broad asset class, but collectively their winning streak extended for a fifth month. Gold head-faked another breakout, turning around and ending down 3.1% for the month. Oil swung for the fences, reaching +15% before settling at a 5.1% boost. Elsewhere, natural gas resumed its levitation trick, rising 23.4% as abnormally cold weather and supply issues emanating from Europe pressured supply. The agricultural commodities were positive as drought concerns and early indications of poor crop quality in the US led to gains of about 7% across the complex.

The uninterrupted upward move in bond yields carried on in April. The US 10-year yield increased 50bps to 2.86%; 2-year yields rose 33bps to 2.64% – an indication that an aggressive Fed will persist throughout 2022 and 2023. Equity drawdowns are logical given experience during periods of heightened economic uncertainly but the degree of weakness in the bond market has few comparables. The Bloomberg Aggregate Bond Index has slumped almost 9%. In fact, one would have visit the late 1970s to find a comparable decline for the index.

The U.S. Dollar continues to be a global wrecking ball in currency markets. The DXY strength was previously a function of its heavy weighting to EUR and JPY which were both faltering. However, in April even the mighty Canadian dollar fell 2.3% while the British pound fell 5.2%. Both the USD and yields have an outsized impact on corporate profitability so these factors will become more prominent in the evaluation of future earnings.

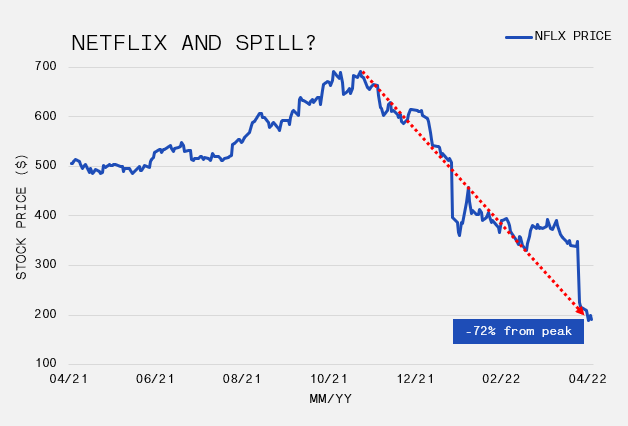

With a new quarter came the start of Q1 earnings season, and so far on aggregate we are seeing results that leave something to be desired. Probably the biggest surprise were the results from Netflix, which left the stock down 35% on earnings day, about 50% for the month and over 70% from its peak in November 2021. The carnage occurred despite beating on earnings and matching revenue expectations. However, investors keyed-in on a drop in global paid streaming subscribers as a sign of competition eating into the aggressive growth expectations that were baked into the stock’s price.

From a macro perspective, US GDP came in well below the estimated 1% growth rate in Q1, falling 1.4%. Upon further investigation, there are some positive signs of economic resilience. First, consumer and business spending remained robust, but this demand was satisfied through imports rather than domestically, while at the same time exports globally contracted. Second, government spending fell 2.7%. The question now will be whether the Fed will use this as an excuse to walk back some of their hawkish talk from May. Or, will they look through the weak headline number and reference the underlying positivity as a reason to continue their tightening program? With equities rising following the news release and yields remaining stubbornly high, it seems bond and stock markets are predicting different outcomes.