August 25, 2020

Lumber and Stocks Extend Gains Through August

Market Recap & Boxscore

The summer of love for equity markets continued into August, led by the S&P 500 which rose 6.5% for the period, breaching its February all-time high. The TSX and MSCI World Indices also registered strong results, but to a lesser degree, rising 3.0% and 3.7%, respectively.

In July, we identified the potential for a sector rotation away from Tech, but this did not materialize in August. The US Tech sector rose 13.7%. It was once again the big companies leading the way, with Apple and Facebook up 31.9% and 20.3%, respectively. FB shook off concerns about reduced ad spending in their Q2 earnings report. Apple combined a strong Q2 with a 4:1 stock split, which gives retail investors the illusion that the stock is suddenly trading at a 75% discount. The logic that a pizza cut into four or five slices does not change the size or value of the pizza, seems to get lost when the pie is stock in Apple.

Interestingly, for much of 2020, Financials, Energy and Industrials withered while tech stocks bloomed. However, Energy was the only one who languished over the past four weeks. Consumer-related stocks have also surprised to the upside as the sector reported reasonably staunch Q2 earnings. For example, Foot Locker beat estimates as comparable store sales were up 18.6% in Q2, while a return to profitability helped to reinstate their dividend. More recently, Dick’s Sporting Goods similarly reported a 20.7% increase in same-store sales and reinstated their dividend. Both companies have benefitted from a rapid rise in online sales. Further, the ongoing rationalization of their store footprint, advanced in Q1, which helped boost margins and net income. It seems clear that despite record unemployment and a continued rise in defaults, the consumer remains strong due to fiscal support.

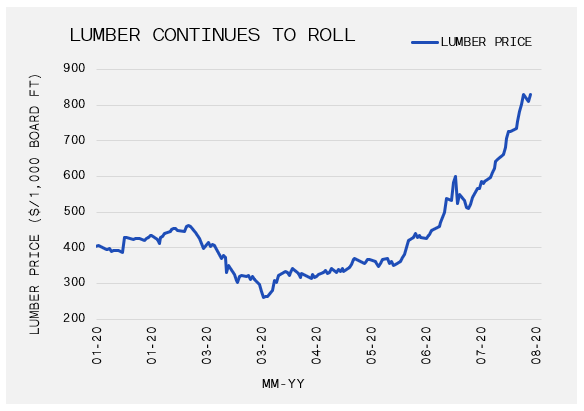

The sustained bid for commodities continued throughout August. Lumber lead the way, sporting a 46% leap during the period, adding to a cumulative 219% return since its 01-Apr-20 low. Elsewhere, the CRB Raw Industrials Index rose another 3.4% during the month and WTI oil ticked up 3.7%. While another 0.7% drop in the USD as measured by DXY continues to be a tailwind, the effects of capacity reductions across producers throughout their long-term bear market are also a factor. While many believe this is a short-term phenomenon with capacity expected to come back online quickly due to price strength, it is not that straightforward. Lumber capacity for example was hit from both the supply and demand side, and while demand has come back strongly from renovation and homebuilding activity, the supply side is more difficult to address. In Canada, producers have exhausted the excess supply of lumber caused by the Mountain Pine Beetle, and government restrictions have limited access to additional supply. Excess capacity south of the border will become accessible in response to record lumber prices. Nevertheless, these price level will have durability if demand remains strong.

In the precious metals space, silver accelerated another 7.9%, while gold prices paused (-0.7%) after a 10.3% surge in July. Even though softness in the US dollar and recovering commodities are promoting the inflation narrative, the 10-year US Treasury inched up 7bps. Yet, the 5 and 10-year US real yields fell 22bps and 11bps to -1.3% and -1.0%, respectively. We remain vigilant with respect to real yields, especially with yields near all-time lows and volatility awakening in the fixed income universe.