June 27, 2021

Federal Reserve Applies Its Influence on Markets

Market Recap & Boxscore

Equities registered another positive month. The TSX repeated as the front-runner, rising 2.2%, followed by the S&P 500 and MSCI World Indices with gains of 2.1% and 1.1%, respectively. Energy continued to pace the TSX, as WTI Oil climbed for five consecutive weeks. The global re-opening is driving demand while a supportive OPEC and reduced supply from US shale producers have conspired to reduce inventories. Further, demand is supported by the prospect that the European re-opening will strengthen. Meanwhile, ESG concerns are expected to restrain future supply. Accordingly, supply-demand dynamics seem to suggest oil prices will advance. However, OPEC may be induced by attractive prices to release reserves which would temper near-term momentum.

Looking forward, it appears the equity markets are poised to grind higher. Benchmark levels are weaving along all-time highs in an environment characterised by low volatility and tight credit spreads. The VIX hit a new post-pandemic low of 14.02 to end the month while the BofA US High Yield OAS index continues to ride the post-financial crisis low, barely budging even during periods of equity weakness.

Despite equity strength, commodities (excluding energy) tumbled since peaking in May. Predictably, the long side of the commodity trade became overcrowded at the top. As a result, outflows intensified in the most extreme positions when the market was bereft of positive news. Copper was down 5.4% in June and 12.1% from its high. Corn and soybeans are off 15.9% and 20.8%, respectively. China has been accused of triggering the downturn. In addition to deleveraging the economy to slow growth, China announced a planned sale of their strategic copper reserves. Thereby becoming a supplier rather than a major buyer across the commodity complex.

Gold’s recent strength was also tripped in June, falling 6% following the Fed’s announcement discussed below. In short, the prospect for higher rates, would curb inflation and widen real rates, which is seen as a headwind for gold prices.

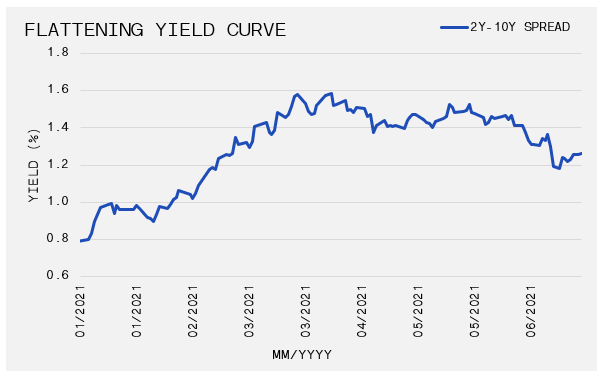

This month’s Fed announcement caused quick and aggressive moves across markets. On 16-Jun-21, the FOMC announced the timing for tapering could be sooner than anticipated and that rate increases might arrive as early as 2022.

In the February 2021 edition of the Recap & Boxscore, we discussed the potential for downward pressure on short term rates because the US needed to spend much of the $1.6 Trillion in the Treasury General Account (TGA). When money leaves the TGA it pumps liquidity into the banking system, in this environment, it threatens to make short-term interest rates zero or below. To avoid negative rates, the Fed increased the rate that is paid on excess reserves by 0.05% to 0.15% at its recent meeting. This action, along with the threat to adjust rates higher, was perceived as hawkish, because it helps reduce the outflow from money market funds into longer-dated bonds, equities, commodities and so on, further inflating bubble-like markets. Nevertheless, long term rates were forced lower because potential tapering would suppress economic stimulus. Consequently, after the FOMC statement, the yield curve flattened, long-term bonds strengthened and Growth Stocks outperformed Value Stocks, as one would expect in a less expanding economy.

As we move into the second half of the year, inflation and GDP comparisons will become a bit tougher. Therefore, interpreting upcoming data prints will be paramount to tactical asset allocation decisions. A particular interesting development will be the after-effects when 21 states peel away Federal unemployment benefits. These states want to incentivize citizens to return to the workforce ahead of the pandemic response program’s September expiry date. Based on data from the Department of Labour, over three million people will lose an extra $300 per week from late June and beyond. As these individuals return to the work force, employment data could surprise to the upside. An expanding workforce would re-ignite the steepening trade that has dominated most of 2021; and reverse the events of June where the flattening curve sparked the excess returns in Growth Stocks.