February 26, 2020

Coronavirus Fears Sweep Through Markets

Market Recap & Box Score

With three trading days left in February, it looks like we will see our first monthly decline across global equity markets since August 2019. As we entered February, the New Year began just as 2019 ended. Confidence surged as macro-headwinds were easing, manufacturing data appeared to be stabilizing, and most importantly, the dynamic duo of the US Fed and Trump would be able to keep markets levitated at least until the election. Then a potential black swan in the form of the Chinese novel coronavirus crashed the party, spooking markets and sending the S&P 500 and MSCI indices down 5.6% and 5.9%, respectively. The TSX has fared better as a 5.6% rise in the value of gold has helped temper the fall.

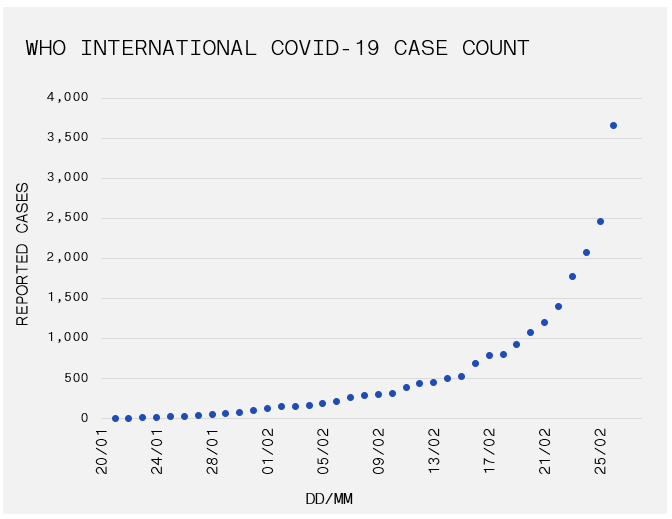

Before Chinese New Year, markets became doubtful that the government could contain the outbreak. Nevertheless, official reports from China gave the impression that restrictions on the movement of about 50 million people were limiting the spread of the virus. Unfortunately, the international case count delivered on 20-Feb-20 disclosed that the spillover was accelerating. By 25-Feb-20, the number of daily new COVID-19 cases outside China exceeded those inside the country for the first time, according to the World Health Organization.

Whether or not the human implications will be as large as some are forecasting is up for debate. Nevertheless, less debatable is the economic implications that have and will come about as supply chains continue to be disrupted. Corporations grind to a halt as their workers undergo quarantine and are correspondingly forced to lower their guidance. Apple was the first market darling to announce revisions on 17-Feb-20. Mastercard lowered its outlook on 24-Feb-20, and its stock price promptly responded with an 11.3% correction. This will surely not be the last corporation to hint at the virus’s impact, and both the severity and duration of the virus’s spread will continue to drive the market in the coming weeks and months. The combination of worries has offset a fairly strong Q4 earnings season. Investor focus will shift forward to discount the potential implications of a sustained global loss of demand, and the subsequent impact on an over-levered and under-prepared corporate sector.

Certainly, equities have taken their lumps, but commodities (ex. Gold) are absorbing the full impact of the fear trade. CRB Commodities Index is down 9.7%. Oil has led the decline with WTI and Brent crude falling 15.3% and 16.0%, respectively. The demand destruction from the world’s second largest economy, and potentially globally, has crushed crude prices and energy stocks. Copper similarly experienced a 9.3% drop; although, interestingly it has stabilized since 31-Jan-20.

Meanwhile, bond yields are being bid to record lows as money flocks to fixed income during the coronavirus scare. Fundamentally the move makes sense. As growth and inflation expectations moderate, bonds become more desirable. Nevertheless, quick and substantial action on behalf of central banks is being initiated to soften the economic impacts of the virus. The Chinese government has already begun to pump monetary and fiscal stimulus, announcing over C$300 billion for special re-lending funds to companies who are reporting 50-60% operating capacity. Hong Kong announced a $15.4Bn package which included a HK$10,000 (~C$ 1,700) payment to every permanent resident 18 and older. Treasuries seem to be forecasting a similar reaction from the US Federal Reserve to help stem any loss of economic strength. It remains to be seen if these activities will help the economy bounce back, but JPMorgan Chase prophesised that China would grow 15% in 2Q19 on a quarter-on-quarter, annualized basis.

Interestingly, on the surface, the Chinese market has not looked back since 01-Feb-20 with the Shanghai Composite Index rising 10.2% month-to-date, essentially wiping out prior weakness. In addition, many areas previously on lock-down have restrictions lifted over the past week as Chinese authorities shift from total quarantine to monitored surveillance. Again, it is difficult to determine whether this is the result of a genuine health improvement or economic desperation … only time will tell.