April 29, 2021

Commodity Bull Rages

Market Recap & Boxscore

Gains were achieved in April across most global markets. The S&P 500 lead the way, up 5.9%, followed by the MSCI World at 5.4%, while the TSX lagged at 2.7%. The Energy sector was the primary headwind for the Canadian market. It is worth noting that these impressive results were registered despite Archegos’s large-scale blow-up (discussed below), global Covid re-emergence, and rumours of the US Fed tapering faster than expected.

In fixed income, yields backed-off of their 2021 highs. The US 10-Year fell from 1.71% to 1.54% but has recovered to 1.63% as the month wound down. However, Canadian long-term yields diverged and continued to rise as the Canadian central bank bucked the global trend of accommodative policy. We anticipate that inflation readings will reflect the economic re-opening, structural shortages and supply chain de-globalization. As a result, the upward momentum in US yields should eventually resume, but our positioning will be tactical and data dependent.

Likely related to falling yields, gold caught a bid in April, rising 5.3% to $1,775. This will be the first monthly gain for the yellow metal in 2021. The gold price faltered in the first quarter as US Treasury Yields gained, the economic outlook brightened and speculative money chased crypto currencies and other risky assets.

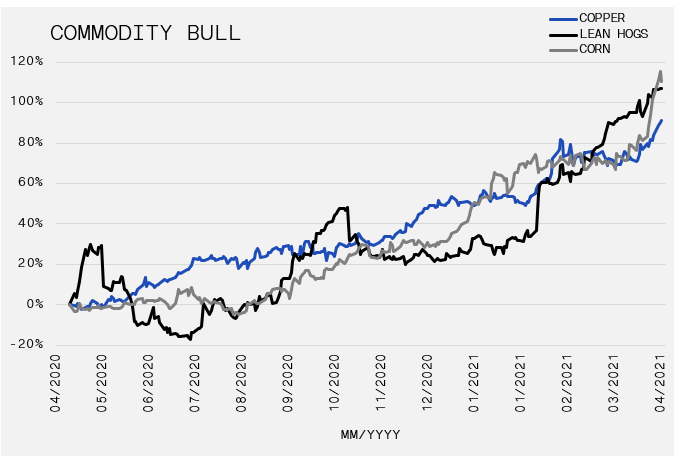

The commodity price rally is widespread, from grains and meats to industrial metals. Our readers are familiar with lumber headlines. In April 2020, lumber was priced under US$260 per board foot. It will close this month near US$1,500. Certainly, accelerating commodity prices are attributed to expectations of a post-COVID demand recovery that outstrips supply after years of underinvestment in capacity. But it is hard to ignore the simultaneous fall in the US Dollar, which is sharply down over 9% on the year. Similarly, the Canadian Dollar continues its torrid pace, up 2.2% in April despite energy weakness, and 14.5% year-over-year. The big move came on 21-Apr-21 when the Bank of Canada became the first central bank to announce tapering of their quantitative easing program, reducing their bond buying program to $3Bn per week (from $4Bn), while also signalling their intention to pull forward interest rate hikes to the first half of 2022. Canada’s ties to commodity prices may have spooked the Bank into believing a more harmful inflation threat was imminent. Alternatively, the Bank may be attempting to cool the red-hot housing market. Regardless, it is difficult to comprehend Canada’s willingness to act first, especially following an extremely accommodative budget, which is sure to leave the country with excess debt to service. Obviously, recent history lessons suggest that any announcement of tightening should be taken with a grain of salt, but in the meantime CAD currency is buying it.

Earlier in April, the frontpage belonged to Archegos Capital Management, run by Bill Hwang. On 26-Mar-21, rumours started to swirl of large-scale forced sales of companies from Chinese tech to Viacom and Discovery, previously boring telecom giants that had run up between 150%-160% in 2021 alone by 20-Mar-21. It later became evident that both the run-up and fall were driven through bank-provided leverage on behalf of their prime brokerage units, whereby the bank provides exposure to the gains or losses of the security in exchange for a set rate, called a Total Return Swap (TRS). This allows the investor to gain exposure to a name without putting up the capital to buy it outright or require ownership to be reported. While TRS is not unique, providing a family office as much as 10x leverage to gain equity exposure of up to $100 billion is nothing short of reckless. Even more so when the office is run by a convicted fraudster. At least eight banks were guilty of the careless loans. Credit Suisse accepted first prize for the greatest misconduct. It reported a loss of $5.5 billion associated with Archegos. Nomura ($2.3Bn), Morgan Stanley ($991MM) and UBS ($774MM) were runners-up. As with any blow-up on Wall Street, more details will become public over time. Some have speculated that Hwang was one of the primary players involved in GameStop and other high short-interest stocks originally attributed to Reddit. 2021 has seen no shortage of ‘interesting’ stock movements so we curiously wait for the craziness to be properly chronicled, while monitoring for any associated risks.