January 01, 2020

Central Banks & Easing Trade Tensions Support Stocks into 2020

Fourth Quarter 2019 Newsletter

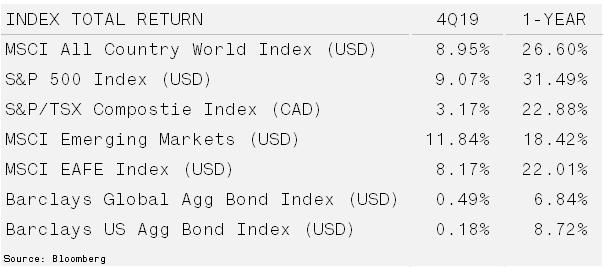

Stocks Accelerated Into Year End – The final quarter of the decade delivered impressive returns as trade tensions alleviated between China and the United States. The S&P 500 experienced its best annual performance since 2013 while Canada’s benchmark posted its biggest percentage rise since 2009. The improved global economic data combined with a weakening US dollar sparked a year-end rally in Emerging Markets.

The US Treasury Yield Curve began to steepen in the fourth quarter. The Federal Reserve cut short-term interest rates in October for the third time in 2019. Investors felt the impacts of easy monetary conditions with an improving economic and inflation picture. The 10-year Treasury yield ended the year at 1.92%. The Bank of Canada bucked the global trend and chose to keep their target rate steady.

Can Ample Liquidity Overcome the Risks in 2020? – The remarkable returns in equity markets for 2019 were not driven by strong earnings growth. In fact, sales growth slowed while costs accelerated. This applied pressure on margins, causing overall earnings per share to remain flat. Despite this headwind, global markets surged to new all-time highs on multiple expansion. Investors were willing to pay more per share for a dollar of earnings.

Multiple expansion typically signifies higher growth prospects or at the very least improving economic and financial conditions. In this instance, multiples were extending because more than half of central banks cut interest rates in 2019. This was the largest amount of easing since the 2008 financial crisis. Monetary conditions were relaxed in response to persistent weakness in global manufacturing. The sector recorded its longest downturn in seven years.

The combination of low but improving growth with loose monetary conditions benefitted the Growth style of investing over value-oriented strategies. Furthermore, passive investing continues to constitute more of the market. As such, the valuation premiums enjoyed by large, liquid companies over lower float, less liquid, smaller capitalization companies should endure.

The “phase one” trade deal between the US and China may help restore corporate confidence. If management teams are more comfortable making long-term investment decisions, capital expenditures will boost revenues. The timing might even coincide with a rebound in global manufacturing which will also lift corporate profits.

With loose monetary policies, peace in the trade war and improving prospects for corporate spending, investors are anticipating an earnings recovery over the next few quarters. However, the threat of inflation and the US election cycle may extinguish the flicker of hope as the year progresses.

If the manufacturing sector has troughed and loose monetary conditions boost growth, the economic slack that restrained inflation may be eliminated. This would force the Federal Reserve’s hand into raising rates. In 2018, the Fed executed too quickly, and markets faltered. Inflation may arise from an energy shock, for example, if tensions rise between Iran and the US; or, from food prices, which are vulnerable to climate change, higher oil prices and a depreciation in the USD.

As for the election, if leftist economic policies gain support and either Bernie Sanders or Elizabeth Warren win the Democratic nomination, markets will be spooked. These policies are likely to hit at the heart of the current economic cycle, hurting corporate profit margins of large firms.

On balance, the bull-market appears to remain intact in the very short-term with ample liquidity, neutral expectations and reasonable valuations. As the calendar advances, we expect to become less constructive on risk assets. Our bond outlook remains steadfast and is summarized in our January 2019 Outlook.