Opportunity in Canadian Oil & Gas Names

The market turnaround that started in March continued into April with global markets rising in tandem. The TSX led the way again in April, up 2.0% on strong commodity performance, particularly oil, with WTI recording a 4.7% gain to follow the 5.4% gain seen in March. The MSCI World (USD) gained 1.4% and the S&P 500 1.0% as earnings season kicks off. So far, the season has been a positive one, with 79.4% of companies that have reported exceeding estimates, according to FactSet. Oil’s move helped drive the 1.8% increase on the Bloomberg Commodity Index for the month, offsetting weakness from soft commodities dragged lower by an appreciated USD. As measured by DXY, the USD was up over 2% during the month, stemming some of the weakness that began in late 2016. Aluminum was locked into the centre of Russian-related sanction headlines. The US imposed sanctions on Russian billionaire Oleg Deripaska and several companies which he has influence on, including Rusal, the world’s second largest aluminum company by output. The prospect of such a large volume of US imports coming offline initially forced aluminum prices to their highest level in six years. However, Mr. Deripaska agreed in principal to relinquish control by selling his stake below 50%, allowing prices of aluminum to drop over 10% on 27-Apr on hopes of reduced sanctions.

Rates continue to make headlines, and this month’s breach of 3% on the US 10-year was the first time crossing of the 3% threshold since 2014 where it briefly hit 3.0% before dropping back below 1.5% in Jul-16. However, in 2014 the Fed was still actively pursuing QE and many are watching closely to see what direction it takes in the coming weeks. On the short-end, the 2-year yield adjusted sharply higher during the month to 2.5%, up 56 bps year-to-date as recent inflation and GDP data have increased investors expectations for Fed rate hikes in 2018 (up to 4). While the short- and intermediate-term rates continue to see large moves, the 30-year’s move has been more muted. At 3.1% to end the month, fixed income markets may not be convinced of the long-term growth thesis.

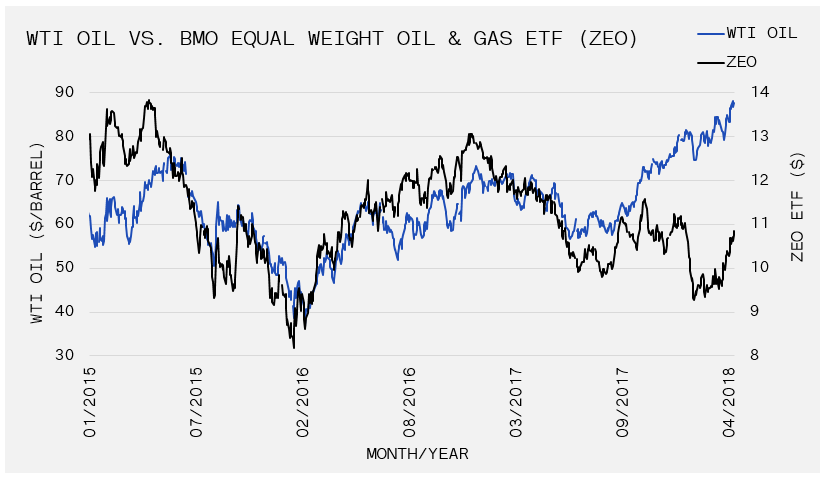

An interesting divergence continues to take place in Canadian oil names. While intuitively, and historically, moves in Canadian oil stocks have followed WTI fairly closely, oil’s rally to end 2017 and into 2018 has not been reflected in the stock prices of Canadian companies in that market. We wrote in Dec-17 about the widened spread between Canadian and US traded oil contracts. However, even after the spread stabilized, it was not until April that Canadian companies started to perform in line with oil, often seeing gains on days that oil saw weakness. Looking at recent price movement and the long-term trend, there may be an opportunity in Canadian oil and gas names that could benefit even if oil stabilizes here.

Monthly Market Recaps