Investors Reposition Assets To Hide From Omicron

Third quarter earning reports lifted equities early in the month until a violent selloff after Thanksgiving Day. For the period ending on 28-Nov-21, the S&P 500 gained 0.9%, while the TSX grinded out a small 0.3% gain as Energy took a breather. The MSCI World Index was the laggard, dropping 1.1% as European weakness led the drawdown. Germany’s DAX Index fell 2.5%. Certainly, the situation with COVID-19 in Europe is much worse than North America. Many countries are recording case counts that far exceed the third wave data. Moreover, Austria and the Netherlands are entering another stage of restrictions and lockdowns.

U.S. stock benchmarks are often dominated by a relatively small number of companies or large cap tech leaders. The top ten positions in the S&P500 represent more than 30% of the capitalization. Predictably, when we look under the hood, we observe that there was limited participation in the uptrend that preceded Thanksgiving Day. Fewer and fewer US companies were trading above their 50-day moving average, which is typically a sign of market fragility. Similar to equities, high yield bonds faltered as month-end approached. The U.S. High Yield Options Adjusted Spread rose from 3.15% to 3.62%. The concentration of Energy issues within the High Yield universe had an outsized impact, but the 3.62% yield is the highest level since March 2021. Access to capital and liquidity have a considerable influence on markets and the economy. The inability to raise money or if the cost to borrow becomes too expensive, businesses become less profitable and unable to expand their workforce, grow their product lines or invest in new opportunities. The current reading is in line with its long-term averages, so it is by no means a sign of long-term market stress – but the trend needs to be monitored.

The Friday after U.S. Thanksgiving is typically reserved for nursing hangovers and analyzing another Detroit Lions loss, but 2021 was different. While US investors still woke up to another Lions loss, there was also a sea of red across equity indices, commodities, and crypto. The Russell 2000 (small-cap stock market index) led the way down, losing 3.7%, while S&P 500 and Nasdaq fell 2.3% and 2.1%, respectively. News of a new COVID-19 variant, Omicron, triggered demand for large cap and tech-heavy indexes, while the reflation/re-opening sectors were shunned. Governments quickly enacted travel bans and momentum for additional lockdowns advanced across Europe and into North America, which caused oil to be the day’s biggest loser, down 12.0%. US Bond performance was equally volatile, with the long-end serving as a flight to safety as the 10-year yield ended the day down from 1.636% to 1.482%. While this was one of the largest one-day moves in recent times, the action at the short-end was even more material as the 2-year yield fell from 0.644% to 0.508%. Yields on the short-end have been increasing aggressively since June as the market anticipated an accelerated pace of Fed tapering and interest hikes. The threat of COVID-induced slowdown obviously tempered these expectations.

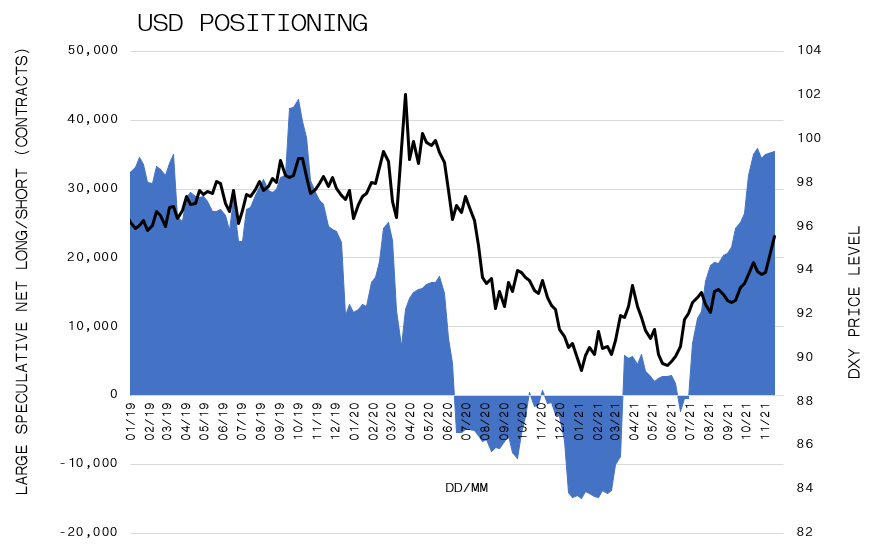

Investor money flows and positioning shifted post-Thanksgiving, particularly in over-crowded areas like the Russell 2000, 10-Year U.S. Treasury Bond and the U.S. Dollar. Russell 2000 had recently become net long as speculators piled into the benchmark. Consequently, risk-takers quickly became sellers as the Omicron news circulated. Similarly, the 10-Year Bond was a popular position for short-sellers wishing to take advantage of the outlook for rising rates. These positions were quickly covered when growth prospects diminished. Most interestingly was the behaviour of the U.S Dollar. The greenback has been propelled higher by large speculator interest. The long position has not been this crowded since November 2019. Typically, when markets falter, investors engage in a flight to safety which causes the U.S. dollar to rise on risk-off days. However, the DXY (the index of the U.S. dollar relative to a basket of foreign currencies) fell 0.7%, a relatively large move down.

Looking out over the very short-term, governments’ response to the new variant and the scientific communities’ reaction to the mutation will likely dictate if investors exercise more traditional re-balancing into year-end or if the Thanksgiving selloff was the onset of a more meaningful correction.

Monthly Market Recaps