How Did We Get Here?

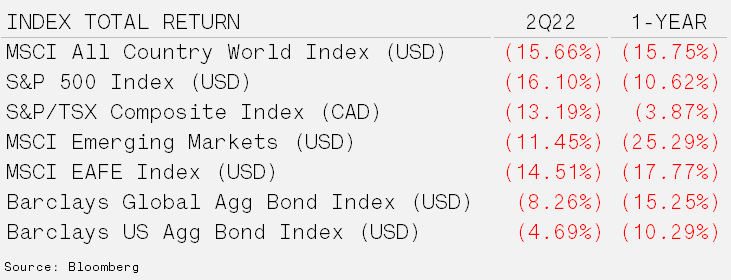

Brutal Quarter Confirms Bear – The S&P 500 entered bear market territory during the quarter, falling 16.1%. Mid-way through June, the benchmark was down as much as 24% from its peak. Persistently high inflation, leading to a hawkish (less accommodative) Federal Reserve combined with an economic slowdown were the drivers behind the weakness. The commodity-heavy S&P/TSX Composite fared much better. However, in the back-half of the quarter, the sectors that were supporting the Canadian index faltered as oil and gold prices lost momentum.

The performance of bonds has been perhaps the more concerning development over the quarter and really the last year. These typically “low risk” investments registered double-digit losses over the trailing 12-months. Late-cycle behavior continues to unfold with wider credit spreads and an inverted yield curve.

The Seven Sins of Inflation – Inflation is a rise in the average cost of goods and services over time. Financial markets measure inflation through the Bureau of Labor Statistics, which compiles data to determine the Consumer Price Index (CPI). The average rate since the Second World War is 3.76%. However, the 10-year moving average is just over 2%. In June, CPI touched a 40-year high of 9.1% year-over-year. Although we continue to believe that structural forces remain in place that make it difficult to maintain a level greater then 4%, it has been the combination of these seven forces listed below that lead us to where we are today. The first two are more long-term in nature and give us the most to think about while the others are supply side shocks, corporate greed, and geopolitical events.

– (1) Rising labour costs in China due to a shrinking working age population and increasing Gross Domestic Product per capita.

– (2) Political forces and capital allocation that favours Environmental, Social & Governance (ESG) have led to under-investment in conventional energy sources.

– The global pandemic of 2020 is responsible for three contributors to the rising inflation prints; (3) trillions of dollars spent in relief packages in the United States, (4) labour shortages as workers left the labour force and (5) supply chain disruptions.

– Public equity valuations are driven primarily by revenue growth and profit margins. Corporations have relied on (6) price increases to stabilize margins to offset rising labour costs and raw material expenditures.

– Finally, (7) the Russian invasion of Ukraine had a direct impact on energy and food prices. Sanctions against Russia removed oil and natural gas supply from the global market at the same time blockades have trapped corn and wheat in one of the world’s largest producing regions.

The factors combating these inflationary forces are mainly structural. The level of national debts, aging populations and a stronger U.S. dollar should alleviate some of the upward pressure on inflation over the long-term. However, it does not appear that we will quickly return to the often cited 2% level of inflation. National interests are now at the forefront of geopolitics. As such, the ESG, supply chain and rising cost concerns overseas have raised awareness of domestic dependence on globalization.

For today’s investors, inflation is vastly outpacing cash savings. Prices double every 19 years based on the post-WWII average inflation rate (3.76%). As a result, protection against the loss of purchasing power for long-term investors is paramount.

Fixed income investments were designed to provide real returns (returns after accounting for inflation) but over indebtedness and lower growth have suppressed long-term yields. Stocks have a mixed track-record when isolating inflationary periods, but in general have held up well. Public market sectors tied to natural resources and real assets have performed the strongest, along with real estate. GAVIN attempts to accumulate these assets during periods of below average inflation when the risk/reward is skewed in our favour. This includes our farmland participation, private and public real estate strategies and commodity investments. Click the link to download PDF version >

Investment Management