Global Stocks Gain Despite Chinese Tech Crash

The S&P 500 recorded its sixth consecutive monthly advance in July, rising 2.4%. The successive gains represent the longest bull streak in 10 years. The MSCI World followed with a 1.8% improvement, while the TSX lagged with a 0.8% increase as energy and financials were weak. While the large cap averages continued their winning streak, there was a notable divergence with US small caps. The Russell 2000 index dropped 3.6%. Investors seem to be flocking to quality, which bid-up the likes of Alphabet (+7.3%), Apple (+6.5%) and Microsoft (+5.2%) at the expense of smaller and more cyclical companies that led for much of 2021. In addition to the tech giants, yield sensitive sectors like real estate (+4.6%) and utilities (+4.3%) had an impressive July. These segments derive much of their worth from either terminal value discounts or a relative yield advantage. Accordingly, their market price has a strong inverse correlation to bond yields, which was beneficial as the 30-year US Treasury yield slid from 2% to 1.89%.

Decreasing bond yields, the weaker tone in small caps and the big tech outperformance seem to be pointing to lower growth in the back half of the year. This is somewhat anticipated given businesses are approaching the point where year-over-year comparisons will start to get tougher. However, we should also highlight that the yield compression is being underpinned by the semi-regular US fiscal ceiling song and dance, which has limited Treasury supply. Further, the Federal Reserve is continuing to buy $80Bn worth of Treasury Bonds and the $1.6Tr drawdown in the Treasury General Account are influencing yields lower.

Despite the slower growth outlook, the CRB Commodity Index increased 2.3% during the month. Natural Gas was the front runner, with a 5.2% surge. Copper reversed its decline since early May and climbed 4.2%. Agricultural commodities stabilized in July, halting the May-June setbacks. The combination of lower long-term yields and higher commodities indicate the market is sniffing out a low growth, high inflation scenario in the final two quarters of 2021. The economic term for this is stagflation, which is typically undesirable because growth is unable to compensate for the higher cost of living. Sustained softness in small caps will support the stagflation scenario and suggest that additional portfolio protection may be appropriate. For example, gold will be attractive in this environment, as its inflation protection attributes are effective during a stagflation setting, which is characterized by flat to falling yields. Correspondingly, gold prices were +2.4% in July as real yields hit all-time lows.

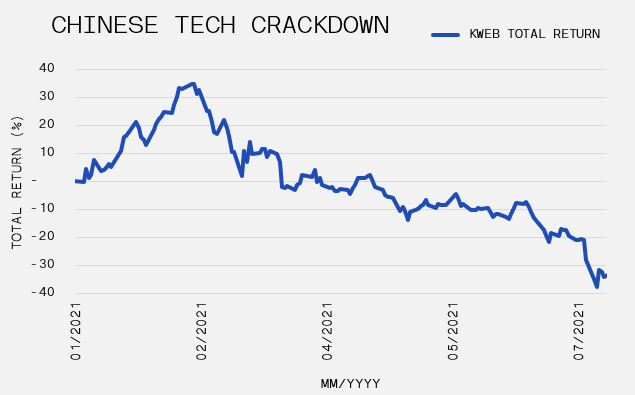

While the action above was certainly interesting, the real fireworks in July were going off in China, as a large-scale regulatory crackdown on technology continues to rage. Chinese tech shares fell 27.7%, as measured by Kraneshares CSI China ETF (KWEB). The price level is 50.3% below its high reached in February. However, the origins of the crackdown began in November 2020, when the highly anticipated IPO from Ant Financial was killed. Ant founder, Jack Ma, who was the former CEO of Alibaba, criticized financial regulators, and the authorities responded by pulling the plug on the initial public offering. Since then, there have been numerous regulatory actions against companies such as Tencent, Didi and Pinduoduo.

Anti-trust laws that were drafted in 2008 are being enforced by regulators during an unprecedented rise in government scrutiny on monopolistic practices in the tech sector. Furthermore, the Chinese government has taken measures to protect the data that firms collect from its citizens. These events resulted in the regime initiating a cybersecurity review of Didi and suspending the ride-sharing app just two days after its US IPO raised $4 billion. Ultimately, the ruling Chinese Communist Party is attempting to harness private enterprise to safeguard the public from increasing inequality and the potential harm caused by gaming, gambling and ideology that is inconsistent with the central government. The country’s $70 billion tutoring industry was a casualty of the intervention. The State Council banned tutoring firms from making a profit – a convincing message that education cannot be dictated by capitalist pursuits. Chinese tech giants, including Alibaba, Tencent and ByteDance, all recently invested in the education sector. Certainly markets are pricing a less tech-friendly regulatory environment in China, but the global impact has yet to be seen.

Monthly Market Recaps