Disruptive Drones and Unrest in Repos

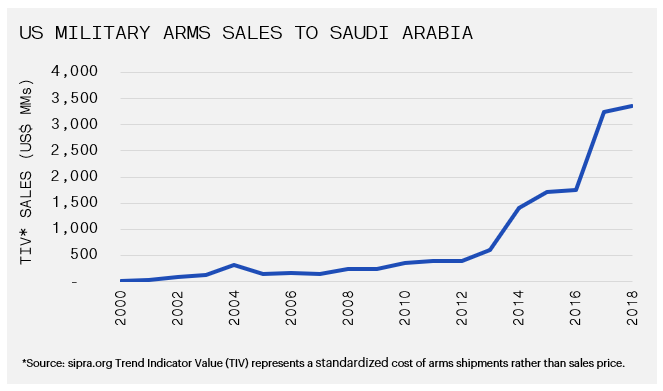

Global equity markets continued their whipsaw action; however, this time the movement was to the upside. The TSX, S&P 500 and MSCI World indices rose 5.4%, 5.3% and 4.8% during the period. A reversal in fund flows supported the stock markets, as recession fears faded and hopes for a U.S.-China trade deal grew. Accordingly, the US 10-year Treasury Yield climbed, initially rising 45bps to 1.90bps by mid-September before moving back down to end the period at 1.66%. Geopolitics returned to the headlines and contributed to the large move in bond yields. The most newsworthy event revolved around the attacks on two major oil facilities in Saudi Arabia on 14-Sep-19. While Yemen’s Houthi rebels claimed responsibility, the US and Saudi Arabia seem convinced of Iran’s involvement. As the accompanying chart illustrates, there has been an alarming growth in military exports of equipment to Saudi Arabia. As such, it is surprising that either Iranian or Houthi drones were able to cause such drastic damage. Recall that in 2017 President Trump brokered an arms deal with Saudi Arabia that was estimated to be worth $350 billion over 10 years. The agreement signified the economic alliance between the two countries and also served as a response to Iran’s malignant activity in the region.

Oil benefited from the tensions in the Middle East as WTI spiked 14.7% on the day. Recently the price has retreated due to reports that the infrastructure is being repaired more quickly than anticipated. WTI finished the period up 6.1%. Bond yields are also responding to the action in oil prices. Oil is a key input for most consumer products and, as a result, it has an outsized impact on inflation. Inflation continues to be disregarded but a turnaround could spark a rout in bond prices.

During the week of 16-Sep-17, it was reported that repo and money market rates shot up to almost 10% on an overnight basis. Repurchase Agreements (repos) are used by banks to handle short-term cash needs. Banks borrow cash overnight in exchange for collateral (Treasury Bonds). Normally, these activities are carried out daily without interruption. However, the temporary spike in rates signaled that banks were short on cash. As such, these entities had to pay a large premium to access cash. The repo rate is influenced by the Fed Funds Rate (FFR), which is targeted to be 1.75%—2.00%. So, it is significant that the actual rate charged for banks to exchange their assets for cash spiked near 10%. Many reasons were cited as the cause for the disruption in the bond market.

There was a large increase of US bond issuance after the debt ceiling was raised in July. Since, banks are the primary dealers, they are legally required to purchase Treasuries with the intention to sell to end users. Consequently, cash had to be used to buy the Treasury Bonds.

Regulations have forced an enlarged requirement to hold reserves at the Fed since the Global Financial Crisis, limiting the ability for banks to provide liquidity in the repo market.

During the Fed’s Quantitative Tightening phase, cash that was previously added to Bank balance sheets in the form of reserves, has reversed and been drained to further stress liquidity.

Whatever the reason, the disorder forced the Fed to re-open their repo operation on an overnight and term basis to become the lender of cash. These measures calmed the market in the short-term, but longer-term uncertainty persists.

For the primary dealers who are buying US Treasury Bonds, is there inadequate investor demand to allow the banks to sell their inventory? Government debt as percentage of GDP has topped 100%, and it will become even higher given the prospect of federal deficits of at least $1 trillion. Is there enough of an investor appetite for more US bonds?

Also, how much capacity does the Fed have to support the repo market? Does this mean another round of Quantitative Easing to stabilize balance sheets and fund the deficits? Besides the Fed, Japan, China, and ETF holders (Vanguard/Blackrock), are the largest holders of Treasuries, so relying on continued foreign investment into the US is critical.

In summary, the cause for the repo market disruption is complicated and wide-ranging. And, ultimately, the short-term consequences may be benign – however, we learned in the Global Financial Crisis of 2007–09 that inadequate liquidity can jeopardize the survival of any bank.

Monthly Market Recaps